After two years, Microsoft still hasn?t delivered on its grand vision for LinkedIn. And it may never do so.

Photo by rawpixel on Unsplash. Logo from LinkedIn media resources.

Photo by rawpixel on Unsplash. Logo from LinkedIn media resources.

Every time this LinkedIn commercial pops up on YouTube I am reminded of how low the company has fallen to.

High school standard slides, accompanied by stock music purchased from Shutterstock.

How did a company like this managed to sell itself for US$27 billion ? at a 50% premium over its last traded share price!

Dumb-ass buyer? Nope, it was Microsoft, under Satya Nadella?s leadership as CEO.

Nadella is credited with turning around Microsoft, after Steve Ballmer?s US$7.9 billion mistake buying Nokia back in September 2013. (The money was pretty much written off by Microsoft in July 2015.)

But did Nadella make the same mistake with LinkedIn, except it would be 3.4x bigger?

A classic case of turning a loser into a winner? for one person.

The only clear winner in the whole deal is Reid Hoffman, the founder and Chairman of LinkedIn.

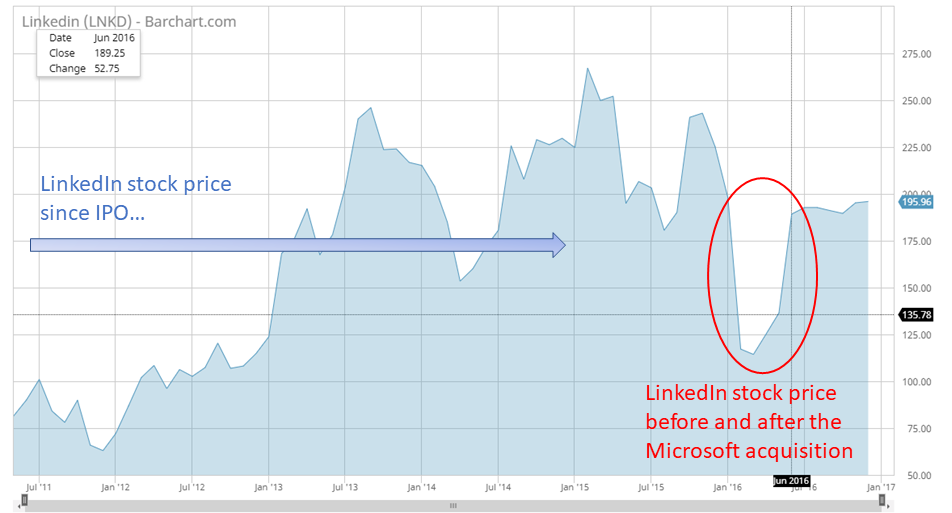

Just four months before the acquisition, LinkedIn?s share price plunged 44% in one day after the company announced a bad quarter and lowered forecasts.

Hoffman lost over a billion dollars in his net worth, which was about one third of his wealth then.

Fast forward to June 13, 2016, LinkedIn announced a merger deal with Microsoft. The stock price shot up by nearly 50%.

Hoffman?s net worth went back up by US$800 million.

Source: Barchart.com

Source: Barchart.com

Four months after the merger was completed Hoffman also joined Microsoft?s Board.

?Inconsistency? would be the word

By all measures LinkedIn wasn?t a great company; even though it kept boasting about its user growth.

Having hundreds of millions of users is pointless if you can?t effectively monetize it. In fact, it becomes a huge cost to keep the platform running and prevent bad user experience due to capacity issues at scale.

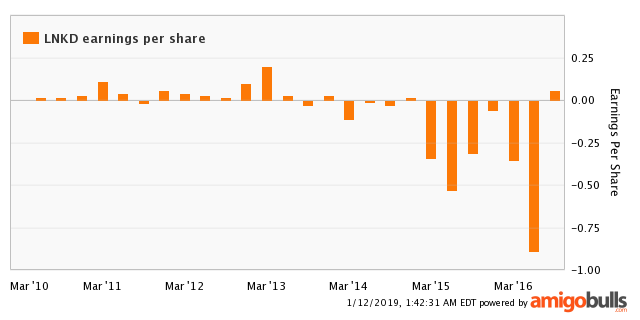

LinkedIn?s historical ability to make money for its investors is as choppy as its stock price.

Source: amigobulls.com

Source: amigobulls.com

But would it be fair to conclude this without taking into account market conditions?

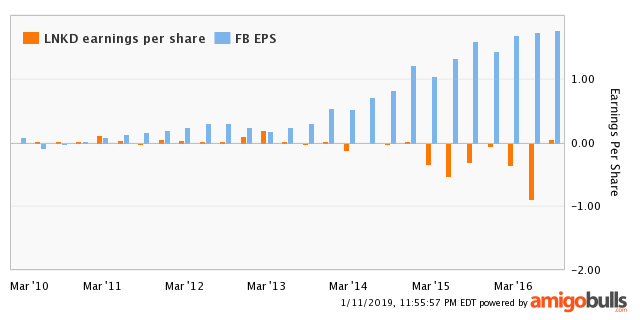

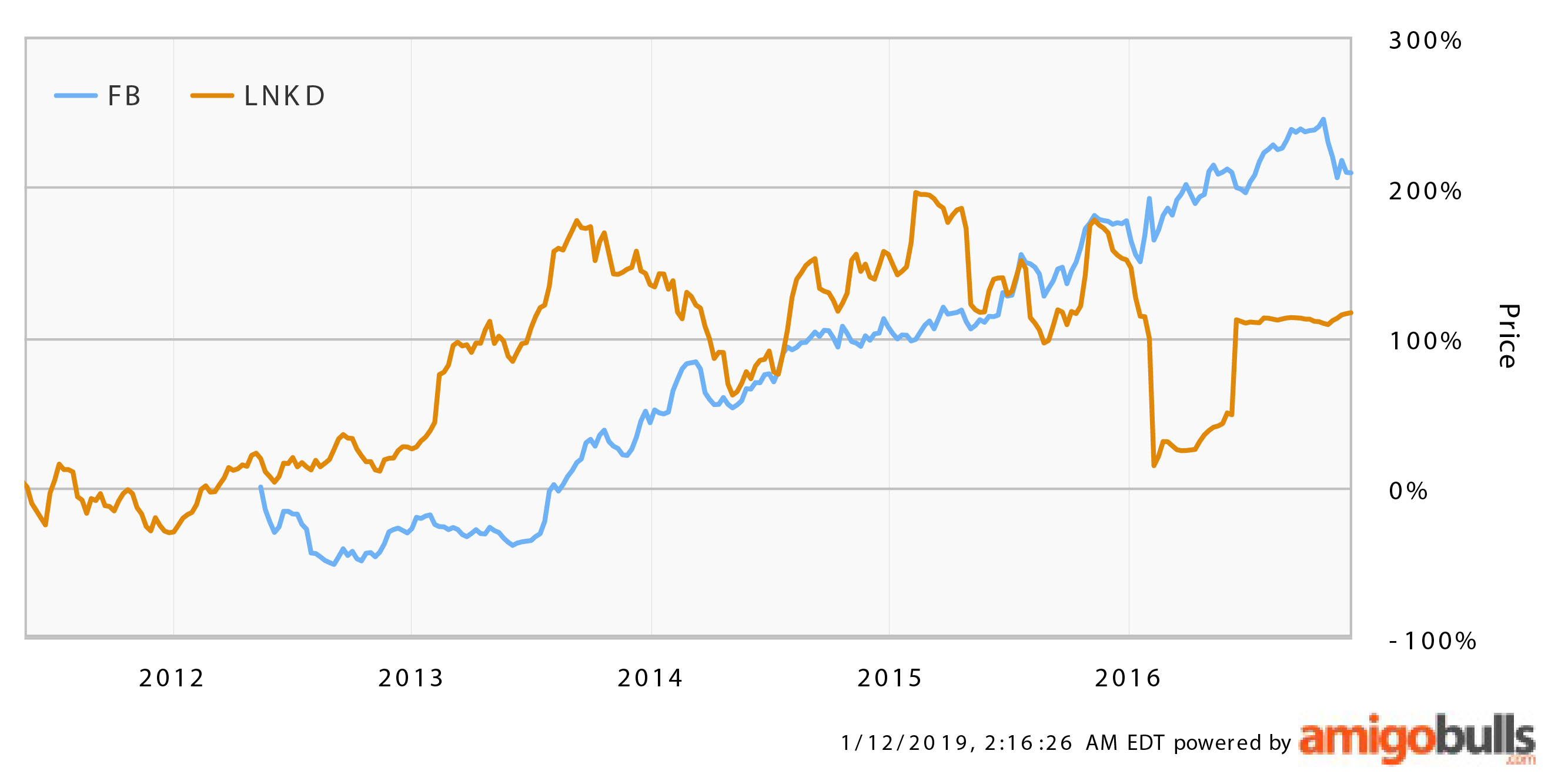

Well, the best comparison to LinkedIn would be Facebook, which was listed almost exactly a year after LinkedIn. Since then its earnings and stock price has steadily trended up, whereas LinkedIn was a constant whip-saw.

LinkedIn vs Facebook earnings per share

LinkedIn vs Facebook earnings per share LinkedIn vs Facebook share price

LinkedIn vs Facebook share price

Was LinkedIn?s turbulent performance bad luck, bad times or bad management?

Where were the problems?

In the aftermath of that 44% stock price plunge, much was written about what LinkedIn?s problems were.

History is history, but let?s look at four which are pertinent to our discussion later.

?Jack of all trades. LinkedIn had ? and still has ? multiple branded apps: Job Search, SlideShare, Learning, Recruiter, Sales Navigator and something call ?Elevate?, which purports to ?build your reputation by sharing smart content?. A news and publishing app called Pulse was integrated into the main app in May 2017.

The idea of selling relevant services to your user base is good, but not if you can?t do it well.

?Bad at integration and scaling. LinkedIn acquired many companies to introduce various services, but wasn?t so good at making them work.

In July 2014 it acquired Bizo for US$175 million to build a B2B lead generation product. That product was scrapped less than a year later. CEO Jeff Weiner said it took ?more resources than anticipated to scale?.

In April 2015 LinkedIn made its largest ever acquisition ? US$1.5 billion for Lynda.com, an online video training provider. In Q1 2016 Weiner again ?acknowledged that integrating and scaling Lynda will require greater investments than previously anticipated?.

?Ads were expensive and user-unfriendly. Natalie Halimi, a marketer with 10 years of experience, wrote about LinkedIn ads back in July 2014. She used the headers ?high CPC, poor dashboard, poor analysis? and concluded ? LinkedIn need to reassess their pricing strategy to provide better ROI for advertisers?.

I too have tried using LinkedIn Ads and compared them to Facebook, Twitter and Google. I have to say I completely agree with Halimi.

?Overvalued, full stop. Just before the plunge, LinkedIn shares were trading at 50x forward earnings. Twitter was at 30x, Facebook 34x and Google 21x. It was one of the most expensive stocks in tech.

Even after the plunge, analysts felt that LinkedIn should be trading at 30% lower to reflect fair value.

But despite knowing all these, Microsoft decided to acquire LinkedIn? at a 50% premium.

Why?

Microsoft?s prescription: remedy or mistake?

Source: LinkedIn media resources

Source: LinkedIn media resources

In an internal email to employees after the acquisition was announced, Nadella claimed he wants to create ?a vibrant network that brings together a professional?s information in LinkedIn?s public network with the information in Office 365 and Dynamics?.

By doing this, he said Microsoft would then be able to detect the project the user was working on and help them connect with ?experts? via LinkedIn to assist them with the task or serve them relevant articles in their LinkedIn news feed.

This begs two very important questions.

One, anyone who uses LinkedIn frequently will know profiles are hard to trust these days. Many are fluffy or even completely fake. How would the experts be qualified?

Two, digging into users? projects provokes personal privacy and corporate secrecy issues. Microsoft tracking what their users do in Office 365? Sounds like a class action legal suit to me.

Nobody I know in big corporates or government organizations has gushed to me yet about how LinkedIn has served up great articles or experts for whatever they are working on in Office 365. I doubt that vision is going according to plan.

The irony is more than thick

Irony 1: If Nadella?s strategy to attract even more Office 365 users via integrating LinkedIn works, it may face monopoly lawsuits yet again.

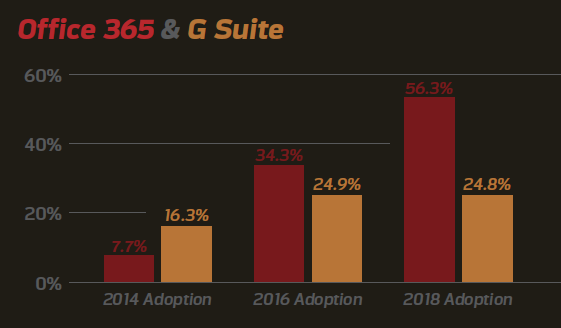

When Microsoft introduced Office 365, it was to battle Google?s G Suite which appealed to smaller businesses with its cheaper pricing and cloud-based subscription model.

It is succeeding. According to a 2018 Bitglass survey, Office 365?s global market share has gone up to 56.3% from 7.7% in just four years. G Suite has stayed at about 25% since 2016.

Source: Bitglass

Source: Bitglass

But?

Creating further success with this strategy by forcing users to use other bundled services will just create the same old legal issue Microsoft had always battled ? MONOPOLY.

Irony 2: Why wasn?t it Google that bought LinkedIn instead?

Here?s an interesting tidbit: LinkedIn?s employees were actually using G suite ? the whole bag: Gmail, Calendar, Drive, Hangouts, Docs, Sheets? ? before the Microsoft acquisition.

So?

Irony 3: Two years after the integration begun, the Microsoft team was still in the process of moving the LinkedIn team over to Office 365.

How could Microsoft possibly convert its worldwide enterprise users to a sophisticated combination of Office 365, Dynamics and LinkedIn when it is struggling itself to move the LinkedIn folks over to Office 365?

And so LinkedIn is facing integration problems yet again with big acquisitions, except now the financial burden is on Microsoft?

Could Microsoft succeed as the (super generous) white knight?

The acquisition was completed in December 2016. It?s been more than two years. How has it been?

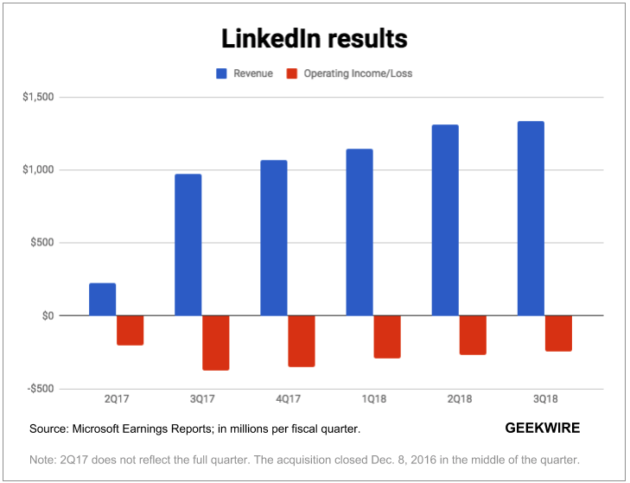

According to Microsoft the acquisition is a big success. It has managed to grow LinkedIn?s revenue quarter after quarter since.

But revenue is all Microsoft ever talks about in its press releases. Why?

LinkedIn is still operating at a loss for Microsoft due to the large amount of intangible assets it has to write off on the purchase ? US$7.89 billion to be exact.

LinkedIn quarterly results since Microsoft acquisition. Source: GeekWire.com

LinkedIn quarterly results since Microsoft acquisition. Source: GeekWire.com

In FY 2017, LinkedIn brought in US$2.3 billion of revenue for Microsoft. But after amortizing US$866 of intangible assets, Microsoft made an operating loss of US$924 million on LinkedIn.

In FY 2018, the situation was the same. Despite LinkedIn?s revenue more than doubling to US$5.3 billion, after amortization of US$1.5 billion Microsoft recorded an operating loss of US$987 million.

The amortization will continue for another 20 years based on Microsoft?s FY 2018 report. Most of the impact will be felt in the first seven years, after which the amount tapers off to about US$107 million per year.

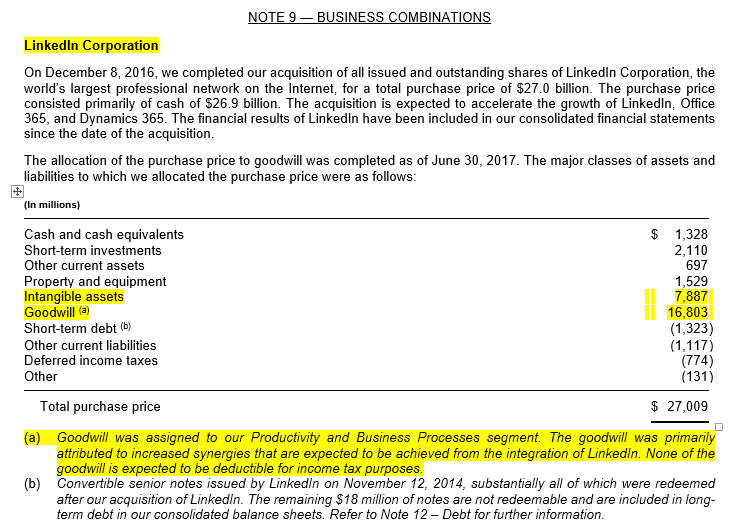

But here?s the REAL kicker. Remember the part earlier where Microsoft paid a 50% premium for a company that was hardly making any profits before the acquisition? Well, that means it pretty much bought a company based on conceptual ?Goodwill? and not actual value ? US$16.8 billion worth to be exact.

Source: Microsoft Q4 FY 2018 10K Report, pg. 75

Source: Microsoft Q4 FY 2018 10K Report, pg. 75

In layman terms, what this means for Microsoft is, even after the US$7.89 billion has been completely amortized, it is still making a loss of US$16.8 billion on the acquisition.

It doesn?t take any more number crunching to realize that Microsoft has a huge task ahead of it to prove the price it paid for LinkedIn was worth it.

And I think Microsoft?s shareholders have came to the same conclusion.

Put your money where your mouth is

In October 2018, Microsoft said in a regulatory filing that activity on LinkedIn will be one of six factors which will be used to determine how much performance stocks Nadella and four other top company executives get.

Performance stocks accounted for one-third of Nadella?s compensation in FY 2018. The tracking will take place over a 3-year period and the payout will only be given in 2020.

At first glance binding Microsoft?s key leadership to the performance of LinkedIn made perfect sense. After all, it was the largest acquisition the company had ever made.

But consider this:

When the acquisition was first announced, Weiner said that Nadella promised him LinkedIn would be operated as a ?fully independent entity?.

Well, Weiner reports directly to Nadella under the terms of the deal. How independent can your decisions be when your boss?s bonus depends on you now?

From left: Jeff Weiner, Satya Nadella, Reid Hoffman. Source: LinkedIn media resources

From left: Jeff Weiner, Satya Nadella, Reid Hoffman. Source: LinkedIn media resources

So it is indeed strange that this compensation scheme was not imposed on Hoffman and Weiner but Nadella and his C-suite instead.

Even more strange is why Microsoft?s compensation board weren?t concerned about user activity not translating into actual profits for LinkedIn.

The metric being used is bizarre. Microsoft will count the ?number of times logged-in members visit LinkedIn, separated by 30 minutes of inactivity?. So that?s basically how often me and other LinkedIn members open our LinkedIn mobile app or visit its website.

How does that translate into LinkedIn being able to make more money? Other than perhaps create the chance to deliver more ad impressions?

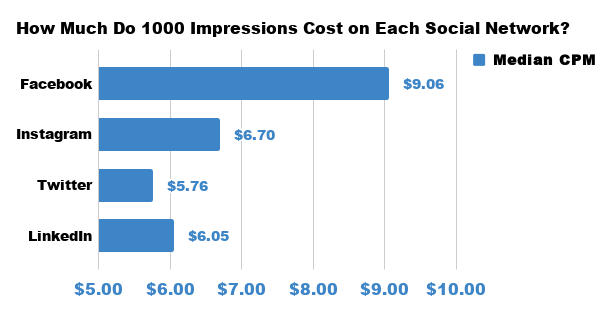

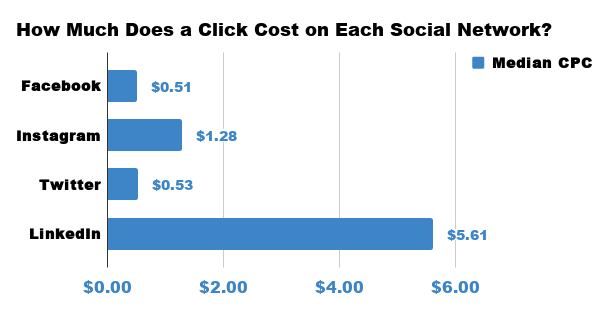

But Cost Per Impression (CPM) is already pretty competitive compared to rival platforms according to one study for 2019. It is Cost Per Click (CPC) that is still stubbornly high for LinkedIn.

Source: falcon.io

Source: falcon.io Source: falcon.io

Source: falcon.io

Indeed, there is no transparency as to how LinkedIn?s revenue has grown quarter after quarter since the acquisition. LinkedIn is now reported as a product under Microsoft?s ?Productivity and Business Processes? segment with few financial details given.

In any case, the pressure is on for Nadella and his team. 2020 is coming soon, and it could be either pay day, or pain day.

Author?s note: This article is exactly one year old as I write this. It has garnered 229k views and has been shared across the world in various languages. Ironically, the social media where it went most viral was LinkedIn itself.

A big thank you to all my readers. It is quite something to see your own article next to WSJ and New York Times on digg.

{kind=link}

{kind=link}